First Principles thinking is one of the most powerful operating tools a modern CFO (or any leader) can wield. This is especially true during times of uncertainty or to simply separate the signal from the noise. Use it to create clarity from the otherwise confusing, unfocused “rabbit-holing” that drives everyone crazy.

We only learn by taking something apart, testing the assumptions, reconstructing it, and then testing new assumptions. In other words, continually course-correcting.

This is where you can lean on Powerful Questions, which I’ve also written about extensively.

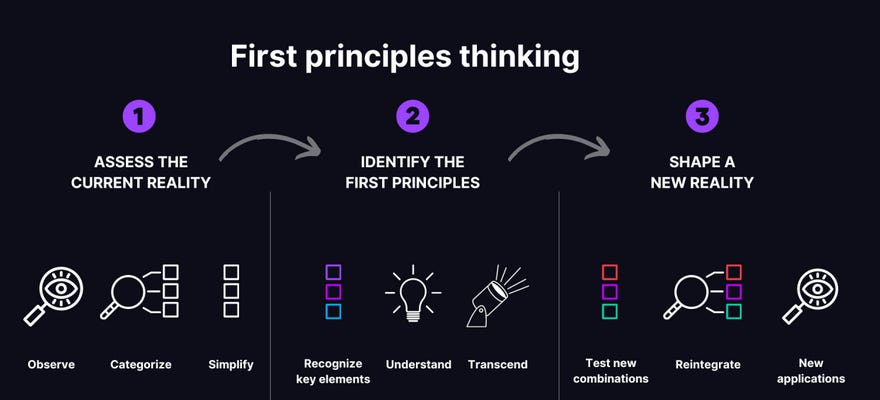

The First Principles Framework

Clarify your thinking and explain the origins of your ideas

Key Questions: Why do I/we think this? What exactly do I/we think?

Challenge the assumptions

Key Questions: How do I/we know this is true? What if I/We thought the opposite?

Review data / evidence

Key Questions: Do I/we have evidence to back this up? Data sources?

Consider alternative perspectives

Key Questions: How do others think? How do I know I am correct?

Account for consequences and implications

Key Questions: What if we are wrong? What are the consequences if we are?

Question the original question

Key Questions: Why did we think that in the first place? Were we correct?

This Socratic process stops you from relying on your gut and limits strong emotional responses. These powerful questions, focusing on the First Principles thinking process, help you make better decisions.

The CFO’s First Principles Framework

Let’s start with what I believe are the three first principles of CFO decision making:

1. Every Assumption Requires Data...Or Must Be Explicitly Labeled as Opinion

Assumptions aren’t the problem. Untagged assumptions are.

The CFO’s job is to architect the truth layer of the company. And that starts with forcing clarity:

Is this assumption based on actual data? If so, show the source, recency, and frequency. We made up a term at Mozilla for this = “Frecency,”which is the combination of the frequency of recent data.

If you don’t have data or evidence, then simply label it for what it is: an opinion-based assumption. That’s fine, so long as we agree it needs to mature into a data-supported decision over time. It’s amazing what happens when opinions meet real life. They turn into data really quickly!

This labeling turns fuzzy, gut-based thinking into crisp inputs for the next course-correcting decision. It also helps build a living assumption map that evolves as reality catches up.

2. Tag Each Assumption With a Confidence Score

Once assumptions are surfaced, tag them with a Confidence Score. I like to use a % confidence score, backed by the amount of data/evidence.

75%-100% = High Confidence (direct solid data with a consistent trend)

50%-75% = Confident (good data; needs more data points to create a trend)

25%-50% = Low Confidence (minimal validations)

0%-25% = Opinion (we can make this decision, but we need to start measuring)

Confidence tagging forces your team to pause and reflect: How sure are we, really?

It also gives your forecast or decision model built-in metadata, so when actuals diverge from the plan, you know which assumptions to interrogate first.

Think of this as building a self-diagnosing system for your strategic model.

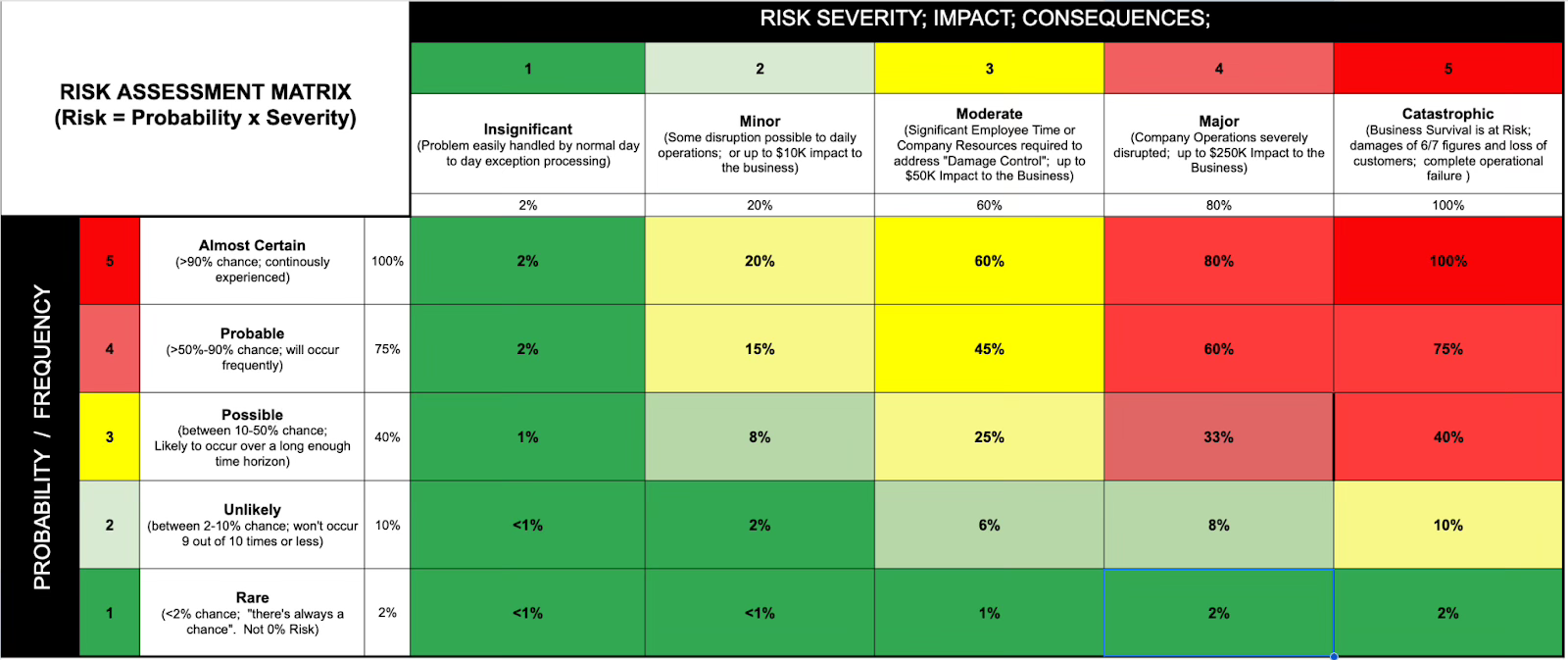

3. Tag Each Assumption With a Risk Score. Use the Risk Equation.

Every assumption carries exposure. Some risks are likely but low impact. Others are rare but could sink the ship. Both need a Risk Score.

So tag assumptions by:

Probability of the risk occurring (Almost Certain vs. Very Unlikely)

Severity of impact (Insignificant vs. Catastrophic)

This helps you focus on the overall decisions with a Risk Score and ultimately helps you prioritize and helps your executive team to focus on not rabbit-holing.

It also prevents teams from treating all assumptions as equally risky or equally confident.

POWERFUL QUESTION: Want to stress-test any decision conversation?

Ask: “Which of our assumptions are both low confidence and high risk?”

The CFO’s Role in First Principles Thinking

Most CFOs are being presented with a "Best Guess" decision stack from their respective teams: “forecasting, innovative initiatives, moving fast”. The CFO’s job these fuzzy decisions into a structured, confident, risk-scoring model. When structured properly, a First Principles framework guides your team to smarter and smarter bets.

Below is the CFO’s PlayBook for putting First Principle thinking to work inside your company. It is for Paid Subscribers only - so become one!

CFO’s PLAYBOOK FOR FIRST PRINCIPLE THINKING BELOW:

Continue reading this post for free, courtesy of Jim Cook.