My ears perked up on CNBC last month during the IPO coverage of ServiceTitan, one of the few high-profile IPO’s of 2024. I thought I’d seen all flavors and definitions of private company investor terms regarding raising startup capital… until the CNBC commentator said “Compound Ratchet”.

Long ago I learned the phrase “You name the price, I’ll name the terms” with respect to what the industry has come to call “dirty term sheets”. In other words, not all money raised is simple or clean. Like pawn shops or bail bonds companies, some terms that come along with raising capital have “hair” or are “dirty”. When you run across complex, hairy, or dirty terms, it’s nearly always a proxy for a mispriced valuation. Why do VC’s misprice a round? To avoid a “down round” and to be able to quote a flat round in terms of valuation price or even a higher valuation vs the last round by simply making the terms more dilutive.

So, I went into research and analysis mode with a hypothesis of post-Covid 2021/2022 term sheet valuations finally being brought to justice through the “emperor has no clothes” transparency that we otherwise know as “being a public company”.

So What is a Compound Ratchet?

A typical ratchet falls into the category of “anti-dilution provisions” and refers to a financial engineering mechanism to protect against a future down round or valuation drops or in more common terms “..somebody getting a better price than me”.

While I was quite familiar with the terms “full ratchet” and “weighted average ratchet”, I’ve not once in my 30 years come across the term “compound ratchet”. After quick research, it is what I feared it was:

A compound ratchet builds an additional anti-dilution layer with multiple and compounding protections. Ouch! In ServiceTitan’s case, the compound ratchet the VC’s wrote into their last round protected against two things:

Time to IPO

IPO Hurdle Price

Time toIPO: Effectively, this term forced ServiceTitan to IPO by making it too painful from an ownership dilution standpoint to stay private. ServiceTitan’s ticking time bomb of dilution was 18 months in their Series H from November of 2022.

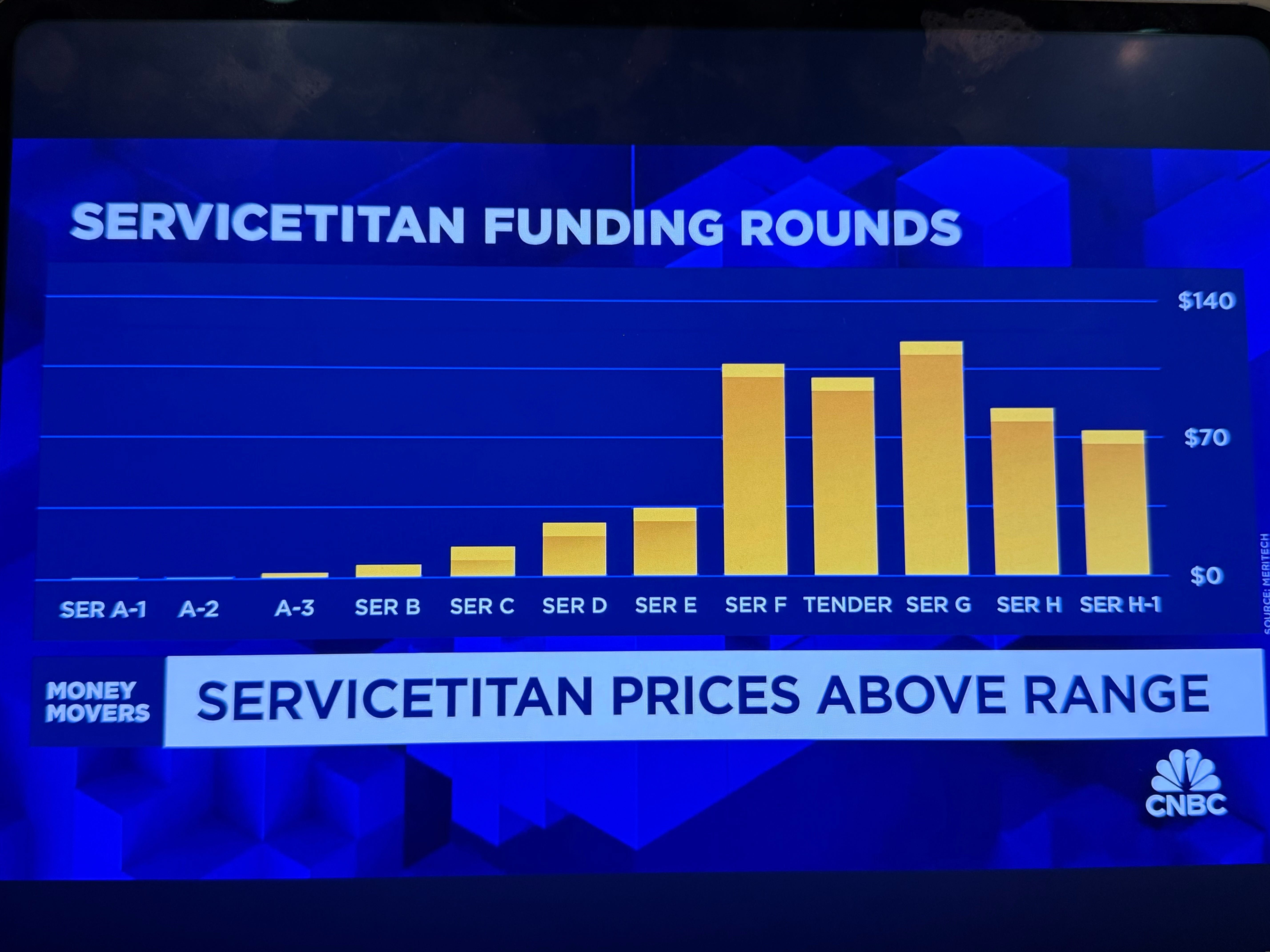

ServiceTitan raised its last round (Series H) of $365 million in November 2022 (source - Pitchbook and Meritech)

The Series H terms said that if the company didn’t go public by May 22, 2024 (18 months later) at a minimum IPO price, the investors would receive more shares that would compound each quarter at an 11% annual rate.

ServiceTitan’s two prior rounds, the Series F and Series G, also had ratchets (but not compounding) at ~$106 and ~$116 per share, respectively. When the company raised its Series H at ~$85 per share, those ratchets were triggered and investors were made whole and had no remaining ratchet on the IPO price.

IPO Hurdle Price: The Series H term sheet in November 2022 set ServiceTitan’s IPO hurdle price at $84.57 a share to avoid having to give the investors more shares. Since we are in December 2024, and the company is past its 18-month window (referring back to step 1 where we discussed the initial ratchet terms), that $84.57 price is now compounding quarterly, and the IPO hurdle price is now closer to $90 a share.

ServiceTitan’s Forced IPO

ServiceTitan was effectively forced to IPO due to these significant investor protections put into place two years earlier. ServiceTitan, like many other unicorns, last raised in the lofty private market valuation class of 2021-2022 faced a “Mortons Fork” of an investment choice:

stay private and dilute yourself away at an 11% compounded quarterly rate.

OR go public as quickly as possible at a price significantly below the IPO hurdle rate.

ServiceTitan's original S-1 IPO price in December of 2024 was printed at $52-$57 per share, then raised to $65-$67 per share, and finally priced at $71 per share. These prices were all well below the $85 per share IPO Price hurdle rate.

Comparing Historical IPO’s: Dropbox, Square, and Others:

I personally drafted my first S-1 in 1993 at Intuit and was fascinated by the document. I’ve been an S-1 “Geek” and have regularly analyzed S-1s of other prominent IPO’s ever since. I distinctly remember a few other notable “Ratchet” S-1s (though they weren’t “Compounding Ratchets”).

Dropbox (2018):

Dropbox, one of the very first “decacorns,” was priced at a $10 billion valuation around 2012. This sky-high valuation made it difficult for the company to subsequently raise money.

By 2018, Dropbox was forced to go public, where its single-layer ratchet was exposed for any price under $10 per share. Eventually, Dropbox also had to employ a reverse stock split prior to its IPO to achieve its IPO Hurdle Price and ended up with significant shareholder dilution.

Square (2015):

Square’s IPO faced similar pressures, pricing at $9 per share—well below its prior private valuation of $15+ per share. Square also had a simple ratchet mechanism, issuing additional shares to Series E investors to make up for any down round at IPO time.

Box (2015):

Box utilized a ratchet to stabilize valuation concerns after multiple delays in its IPO process.

Will We Now See More Compound Ratchets in Future Financings and IPO’s?

ServiceTitan’s disclosure of a compound ratchet may be the canary in the coal mine of the 2021-2022 VC/PE financing class. The IPO market overall is still trying to show signs of life but the rate of IPO’s is still anemic. There have been fewer IPO’s over the last 3 years combined than even the worst single year over the last 10 years as evidenced by this screenshot I took during the CNBC coverage of ServiceTitan’s coming out party:

A total of 15 tech IPO’s occurred from 2022-2024 (3 years!). And I thought 2016's 17 tech IPO’s was the low water mark—no wonder I haven't been reading S-1s lately!

Broader Market Implications:

I’m hoping compound ratchets do not become the norm in a VC market still grappling with the hangover of inflated private valuations combined with the fact of VC-backed companies staying private for over 12 years before going public. Note: ServiceTitan hit the average. It was founded 12 years ago and raised over $1.5B in private capital prior to going public.

1. Down Round or Ratchets? Now that you understand ratchets and even worse, compound ratchets, I suggest Founders, CEO’s, and VC’s may want to think about simply “taking your medicine” and getting back to pricing your private company properly. Is a clean-down round really that bad optically? The public markets go through “down round pricing” all the time. Isn’t the aspiration of all private companies to be public? Why not act like public companies and simply price according to current market rates instead of “hiding the ball” with clever financial engineering terms?

2. Always Look Under the Hood: Founders, Private, and Public-market investors need to understand the actual terms in a company’s prior round term sheets to get a true view of how past investors valued the company. The price of your round is not what matters. The Terms matter more. “You name the Price, I’ll name the Terms”. Never forget it.

3. Are Private Companies Effectively Already Public? We may be facing the reality that the mega later-stage funding rounds are effectively public valuation-type rounds with the advantage of staying private. Evidence is mounting from both current public companies and the ones like ServiceTitan’s IPO that a 25-30% annual growth rate is “good” and more “normal” than the young IPO companies of the past with significant growth rates well beyond 50% annually. If this trend continues, look for IPO Pricing’s to be very similar to or possibly even lower than the last few private rounds since the private rounds already effectively priced them as a public company. This means the days of huge “IPO Pops” many of us have experienced historically may be coming to an end. The market value of a 12+-year-old company growing at 25% annually (the new normal) is much better understood than the IPO companies from 2005-2015 with an average age of only 6-8 years and much higher annual growth rates.

ServiceTitan’s IPO—and its use of a compound ratchet—offers a glimpse into the evolving playbook for tech companies entering public markets. It’s a story of staying private longer, growing slower, and requiring investor protection as a potential new market reality. For founders, executives, and employees alike, understanding not just pricing but the actual terms in a term sheet is a crucial component of any future analysis of a company’s valuation.

With all that said, the overwhelming sentiment is that 2025 is going to be a much better IPO year. In the end, ServiceTitan while suffering dilution ended up “popping” on its first day of trading, gained 40%, and closed its first day of trading at $100 per share (up from its IPO Price of $71 per share). All’s well that ends well, but it could have been a much more dilutive deal for founders and employers if the original $52-$57 price range held.

Key Lesson Learned and Paying Forward?

“YOU NAME THE PRICE….I’LL NAME THE TERMS”

Don’t ever forget it. Read your term sheets. Read your contracts.

For the full rundown details for those finance masochists who want to read more on all of this, Meritech did a great job of it and was my source for the above analysis.

Cook's PlayBooks is a reader-supported publication. To receive new posts automatically in your inbox consider becoming a subscriber. There are both free and paid versions.

This was extremely informative and a high value article. As usual, thanks for the sharpening coach!

Joey Jenkins