The IPO Already Happened

The New Private-Public Company - A “Distinction Without A Difference”

For my entire career and the entire history of Venture Capital, the IPO was the defining financial milestone for private companies.

It was the moment. It was the “graduation event” for private companies. We received “Tombstone Trophies”. We rang the bell. We started doing interviews on CNBC.

Over the last 10 years (from roughly 2015 to today), a massive amount of new money has entered the private company ecosystem (VCs and PEs) which has “slowly then suddenly” fundamentally changed the private company “market” of startups.

In the late 90s, the average time a celebrated IPO company was private before it filed to go public was 4 years.

By the late 2000s, private companies were “staying private longer” and the average was 8 years.

By 2015, the average public company was private for 12 years.

Today, I don’t even track the metric anymore as there simply has been a dearth of actual IPOs over the last 10 years.

But if I had to estimate it, we are approaching 15 years of being private before “going public”.

In terms of money raised at IPO and the market capitalization of companies IPO’ing over the same period? Here’s the data:

Many of today’s greatest companies already went public.

They just “became public” in the private market.

SpaceX.

Stripe.

OpenAI.

Anthropic.

Databricks.

And several others still marching toward the now magical trillion-dollar potential.

On CNBC and other media outlets, these companies and others are talked about as if they are already public.

These companies have already raised capital at scales larger than any IPO in history.

Not millions or billions of funds raised… but now 10s of billions.

Recently, we are now hearing $100s of billions in financing activities for these “private” companies.

Historically, the IPO was where institutional capital filled the scaling requirements.

Today, institutional capital has gone private.

The Private Market Became the New Public Market

Look closely at the cap tables of these late-stage private companies.

They don’t resemble “venture-backed startups.”

They resemble public companies.

Analyzing these cap tables you’ll find:

Sovereign wealth funds

Pension funds

Mutual funds

Hedge funds

Family offices

Cross-over investors

Large institutional asset managers

Massive secondary markets

Structured liquidity programs

And increasingly… retail participation

A vast majority of the retail participation is wrapped neatly in modern cap table packaging called SPVs (Special Purpose Vehicles).

AngelList helped normalize this structure years ago, but now the entire ecosystem has evolved around democratized private-company access.

Retail investors are already participating without the IPO.

A Distinction Without a Difference?

Historically, the IPO served several purposes:

1. An IPO Was The Source For Large Amounts of Capital

Already happening privately.

2. IPOs Created Liquidity

Secondary markets now accomplish much of this. True real-time liquidity, however, can only be found in public markets.

3. IPOs Institutionalized Ownership

This has largely already been accomplished a year before the actual IPO today.

4. IPOs Expanded Investor Access

Increasingly happening through SPVs and private access platforms.

5. IPOs Established Market Price Discovery

Private rounds now happen frequently enough to continuously reprice elite companies.

The old IPO process is no longer the beginning of institutional ownership.

Of these Top 5 IPO reasons today, only real liquidity - ability to buy and sell real-time is the reason to IPO.

Healthier? More Stable?

It can be argued that this private market evolution may actually be healthier for companies.

Giant late-stage private rounds eliminated one of the most dysfunctional aspects of historical IPOs:

The real price-discovery and volatility of first-day pricing pops and lock-up period declines.

For years, Wall Street celebrated IPO “success” when a stock exploded 40%, 60%, or 100% on day one.

But let’s call those IPO pops what they really were: Massive underpricing in the private markets.

Today’s IPOs are more likely to see their day 1 or week 1 prices decline significantly from their private values. The IPO “pop” has been mostly unseen in recent years.

Today’s mega-private rounds operate differently.

The capital is raised:

Behind closed doors

With (theoretically) better price discovery

Across multiple rounds

With (theoretically) sophisticated investors

With structured governance

And with far less speculative day-one frenzy (though speculative VC/PE Frenzy!)

Combined with controlled secondary liquidity, companies can scale with dramatically less volatility.

Cash Liquidity and funding stability creates better long-term execution environments.

The Rise of the “Private Public Company”

We are now witnessing the emergence of an entirely new category:

The Private-Public Company

These companies have:

Hundreds of shareholders

Institutional governance

Massive valuations

Global brands

Mature financial systems

Sophisticated reporting

Deep liquidity ecosystems

Structured employee liquidity

And broad investor participation

Yet they remain technically “private.”

Why?

Staying private is no longer a disadvantage. It’s actually a huge ADVANTAGE!

They avoid:

Quarterly earnings circus dynamics

Activist pressure

Quarterly short-term-ism

Daily retail volatility

Excessive public disclosure requirements

And public market narrative swings

Meanwhile, they still have access to enormous pools of capital that only existed publicly historically.

The Old IPO Was a 1 Day Event; The New IPO Is Multi-Qtr/Year Process

Today, “The IPO” is unfolding continuously over years through progressive private capitalization.

The actual public listing may soon become little more than:

A liquidity expansion event

An index inclusion mechanism

A regulatory and governance transition

A simple PR and branding milestone

Economically?

The new and expanded private markets have already treated these companies as public long ago.

The real question is no longer: “When will these companies IPO?”

The real question is: “What does ‘public’ even mean anymore?”

Private Company Facts:

Massive institutions already own the shares

Retail investors already participate indirectly

Continuous price discovery exists

Secondary liquidity exists

And tens of billions have already been raised…

A.K.A = “The IPO already happened”

The Data Tells the Story

For most of modern venture capital history, companies simply did not stay private long enough — or become large enough — to resemble today’s mega-unicorns.

That’s what makes today’s private company valuations so historically different and why it’s clear today’s largest private companies are “Already Public.”

The Historical IPO Model (1995–2025)

AHA Insight #1: Multiple private companies are now worth more than nearly every historical IPO ever created.

The historic private company financing ladder looked like this:

Seed → VC Rounds → IPO → Scale

The new model increasingly looks like:

Seed → VC Rounds → Growth Equity → Sovereign Funds → Crossover Funds → Secondary Markets → Mega Private Rounds → Why IPO?

AHA Insight #2: The private market has clearly now swallowed stages of company development that historically belonged to the public market.

For complete historical context and perspective, in 1999:

$1B IPO’s Valuations were almost unheard of.

$5B IPO’s Valuations was extraordinary.

$10B+ IPOs, especially technology companies, barely existed.

In the 1990s, a $1B IPO Valuation for a Tech Company was extremely rare.

I believe only 3 companies achieved it [Netscape 1995 ($2.9 Billion); Yahoo ($1.0B 1996; Ebay 1998 ($1.9B)].

Priceline kicked off the Dot Com Bubble/Bust in March 1999 when they hit a never heard of before $10 Billion valuation after the 1st day of IPO Trading.

VA Linux was the poster child of Dot Com Boom/Bust in December 1999 with their $9B of Market Cap on their IPO, achieving the largest 1st day percent gain ever (700% 1st day Pop); IPO Price = $30 per share; Opening trade = $300 per share; Intra-day high $400 per share; 1st day close = $240 per share.

Today’s Private Company Perspective (2026):

Daily and weekly, we are hearing these kinds of valuations of still private companies:

OpenAI $800 Billion

Anthropic $900B - $1.5 Trillion

SpaceX $1.5+ Trillion

Stripe $200 Billion

DataBricks $125 Billion

XAI (formerly Twitter) $60-80 Billion

Private Companies? No, these are “Virtual Public Companies.”

My own personal stories and tracking I’ve done that nearly everyone doesn’t know or has long forgotten.

These stats will blow your mind. I encourage you to take your time in this section.

I recently spoke to a Stanford GSB (MBA) class and shared the stats below. Several asked “Really?” I had to say “Yes, REALLY!”

Intuit: March 1993 IPO

1st day IPO Price $20 per share

$300 Million Market Cap at IPO Pricing (today, companies can’t go public unless they are worth more than $1B+ in the public markets)

Total Shares Sold to Public = 1.75M shares (Jim, are you sure that’s not a typo? Nope - take a close look at my “Tombstone” pic at the very top of this post)

Cash Raised at IPO or roughly $35 million after all fees/greenshoes. (IPO Price $20 per share x 1.7M shares)

$400 Million Market Cap after IPO 1st Day Close ($33 per share; +33%) - there are hundreds of private companies valued at this level today

“4th largest Software IPO Ever” - Headlines in these things called “Newspapers” in 1993 - (no internet, no browsers, no smartphones) - I still have the framed San Jose Mercury News article

Today’s Intuit Market Cap 2026 = $115 Billion

400x Market Cap Increase since IPO Pricing

Amazon: May 1997 IPO

1st Day IPO Price $18 per share

$425 Million Market Cap at IPO Pricing

Total Shares Sold to Public = 3 million shares

Cash Raised at IPO of roughly $50 million

$550 Million Market Cap after IPO 1st Day Close ($23 per share; + 30%)

Today’s Market Cap 2026 = $2.9 Trillion (with a “T”)

6,825x Market Cap Increase since IPO Pricing

Netflix: May 2022 IPO

1st Day IPO Price = $15 Per share

$475 Million Market Cap at IPO Pricing

Total Shares Sold to Public = 5.5 million shares

Cash Raised at IPO of roughly $75 million

$550 Million Market Cap after IPO 1st Day Close ($17 per share; +15%)

Today’s Market Cap 2026 = $375 Billion

800x Market Cap Increase vs IPO Pricing

Google: August 2004 IPO

1st Day IPO Price: $85 per share (Dutch Auction style - labeled a “failed IPO” at the time) - initial S-1 Pricing of $150 per share

$25 Billion Market Cap at IPO Pricing

Total Shares Sold to Public was about 20 million shares

Cash Raised at IPO was roughly $1.7 Billion

$30 Billion Market Cap after IPO 1st Day Close ($100 a share; +15%)

Today’s Market Cap = $4.8 Trillion

200x Market Cap Increase since IPO Pricing

Facebook (Meta): May 2012 IPO

1st Day IPO Price = $38 per share

$100 Billion Market Cap at IPO (absolutely unheard of at the time - crazy several called it)

Zero 1st Day Pop. Stock closed where it was Priced after going up 20% intra-day and then falling by the close

420 million shares sold to public at IPO

$16 Billion of IPO Proceeds (again, crazy and unheard of - see the others above for just how “crazy?”)

Far and away the largest Tech IPO of the time

Today’s Market Cap = $1.6 Trillion

16x Market Cap Increase since IPO Pricing

My take? Facebook was the “come to Jesus” moment for private markets and started the mental narrative of “If FB is worth this much, THEN my portfolio company is worth $Y…” and so the VCs and founders started pricing their private rounds this way.

Our financial markets have clearly evolved but our IPO Language or perspective hasn’t caught up yet.

The next generation of iconic companies may never experience the traditional IPO cycle the way prior generations did.

Because they are “already public” - they just don’t have a ticker symbol whose trades post real-time on the Nasdaq or NYSE.

CFO Guidance for the “Private Public Company”

Your first shift is psychological.

Many executive teams still describe themselves internally as:

“A startup”

“Early stage”

Or “private”

But if your cap table includes:

Sovereign wealth funds

Crossover investors

Mutual funds

Pension funds

Secondaries

Tender programs

And hundreds or even thousands of employee shareholders…

…you are already functioning inside the public capital markets ecosystem.

The CFO must become the architect of that transition long before the ticker symbol arrives.

1. Build Public Company Financial Discipline Early

The best private mega-companies now operate with public-company rigor years before IPO.

That means:

Faster monthly closes

Better forecasting accuracy

Clean audits readiness

Proper internal control and security/privacy controls

Public company investor-grade metrics

Operational rigor

The finance organization can no longer function as a reactive reporting team.

Once your valuation crosses $50B–$100B, the market assumes institutional maturity whether or not your systems are ready.

2. Design a Long-Term Liquidity Strategy

Historically, the IPO solved liquidity. Today, liquidity is continuous.

Employees, early investors, and executives increasingly expect:

Structured liquidity windows including secondary programs and tender offers

RSU type compensation opportunities.

This highlights the CFO responsibility of shareholder and stakeholder relations and doing so without destabilizing ownership structure or culture.

3. Build an Investor Relations Function Before You Need One

Many mega-private companies now manage dozens of sophisticated institutional investors.

Most still lack a true investor relations infrastructure.

This will come back to bite you. Once large institutions enter the cap table:

Communication cadence matters more than ever

Narrative consistency is critical

Governance maturity matters

Guidance and Expectation management becomes a strategic requirement

The modern CFO must increasingly function as:

Company translator

Financial storyteller

Market educator

Even while technically “private.”

4. Operate With Public Market Transparency Internally

One of the biggest risks in hyper-scale private companies is informational asymmetry.

Employees often hold enormous paper wealth but operate with very little understanding of:

Liquidity timing

Valuation mechanics

Dilution

Tax implications

Or secondary market realities

This can create bad actor relationships who step in to try take advantage of the private company investor relations weaknesses.

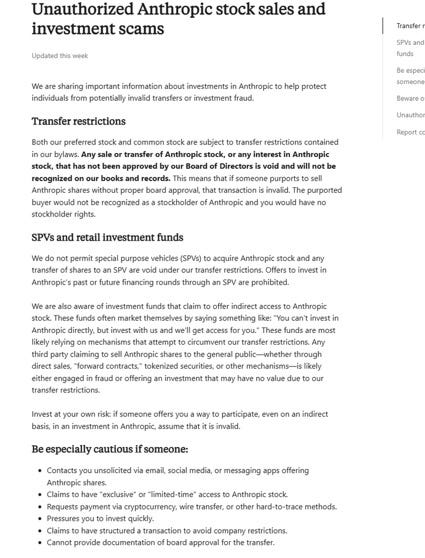

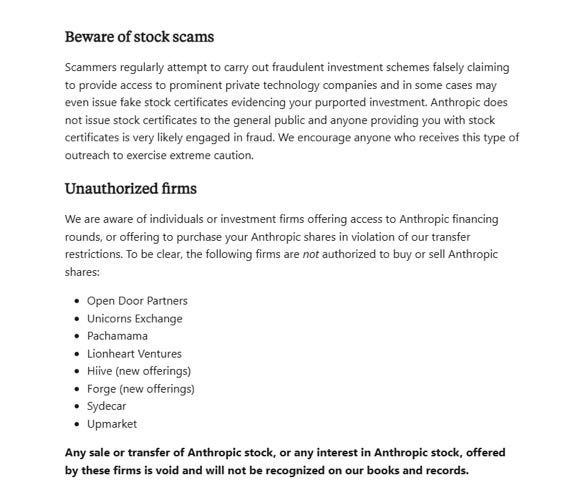

Anthropic just a few days ago dropped a bomb on this very topic

“Any sale or transfer of Anthropic stock, or any interest in Anthropic stock, that has not been approved by our Board of Directors is void and will not be recognized on our books and records.”

Void. Not restricted. Not pending review. Void.

That means if you bought Anthropic shares through Forge, Hiive, or any other secondary platform without board approval, you are not a stockholder. You have no stockholder rights. Your transaction is invalid.

It gets worse. Anthropic says it does not permit SPVs to hold its stock. Any transfer to an SPV is void. Investment funds claiming to offer indirect exposure are “most likely relying on mechanisms that attempt to circumvent our transfer restrictions.” Forward contracts, tokenized securities, synthetic exposure products, all of it potentially worthless.

Their advice to investors: “Assume that it is invalid.”

5. Don’t Confuse Valuation With Durability

This may be the most important lesson of all. Never forget that a CFO’s role is to be the counterbalance to the valuation enthusiasm and to ensure the company can grow into its valuation in a reasonable way.

Private market valuations can now reach extraordinary levels before a company fully proves long-term durability.

That creates enormous pressure on CFOs to separate market enthusiasm from business model and operational model realities.

Because eventually, market valuation fundamentals always matter long term

Final Thought

The modern CFO is no longer preparing companies merely for IPO.

Increasingly, they are managing companies that already function like public institutions while still operating inside private-market structures.

That is a completely new leadership challenge.

And the CFOs who master this transition early will become some of the most important architects of the next generation of iconic companies.

“The CFO Playbook for the Rise of the Private Public Company”

If you thought “IPO Readiness” was a “process” you did 18 months prior to your planned IPO, it’s time to reframe being “IPO Ready” in this new Private Company environment.

Become a paid member of this Substack to get access to my upcoming limited seat webinar (I do these monthly). We’ll have a deep conversation on this topic how to become “public ready” while remaining private.

How mid-to-late-stage private finance teams need to begin mirroring public company finance organizations much earlier than they thought.

Secondary liquidity program design - the “public market” inside private companies.

Tender offers and employee liquidity structures

SPV ecosystem implications

Governance evolution before IPO (Security, Privacy, Audit, Compensation, Board)

The rise of crossover VC investors and how it has created this new environment

The emerging role of private-market IR (Investor Relations)

The new CFO skillset required to manage “private-public” companies